Our valued sponsor

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Estonia e-residency + Portugal NHR

- Thread starter Nikola

- Start date

If you want to take out dividends (or essentially take out money any other way), you pay a 20% tax in Estonia (and maybe something in the country where you are a tax resident, needs checking). For Portugal under NHR seems to be 0% on dividends so far.

It's 20% in Estonia + 10% WHT on dividends as stated in the EE-PT treaty.

Estonia doesn't levy withholding tax on dividends paid to nonresident companies but since you will be receiving dividends under NHR you will likely pay WHT according to the treaty.

I will bring your point up with my accountant in Portugal. But he seemed to suggest that instead of 20% in Estonia, I'd pay only 10%. Then receive the dividends tax free in Portugal. Again, this is where I lack clarity. And it's your version that I am afraid of being true.

I highly suggest you to not rely only on your accountant in Portugal but also to ask EMTA about it because all the taxation will take place in Estonia: [email protected]

And BTW i would trust more EMTA than any PT accountant.

In my experience they are quick to reply.

Please report back your findings.

And BTW i would trust more EMTA than any PT accountant.

In my experience they are quick to reply.

Please report back your findings.

Interesting! I was under the impression from my Tax Lawyer in Portugal that they already have clients who have businesses in Estonia and they are paying 0% on dividends in Portugal under NHR. They didn't mention anything about the 10%, but perhaps I misunderstood. Will check and report back! Thanks for the contact @Marzio !

does this set-up work even if you reside in Malta?If you don't live for 183 days in PT then you could pair your NHR with a US LLC.

You only need to rent an apartment in PT t be considered tax reisdent there so If you don't stay long enough in PT to trigger a permanent establishent then it could work but you have to double chck with a Portuguese lawyer.

In theory it works.

is it necessary to create a substance in the USA? in order not to risk the PE

does this set-up work even if you reside in Malta?

Nope because Malta follow the 183 days rule

is it necessary to create a substance in the USA? in order not to risk the PE

In case of Malta it could be beneficial to manage an offshore company from Malta making it tax resident in malta.

https://corriericilia.com/publications/resident-non-domiciled-companies

Paying the 0% on dividends in Portugal makes perfect sense. But the question is what was their tax rate on the distribution from the company inside Estonia?

Let me know if you find a definitive answer! Also looking into this.

My Portugal accountant believes Estonia + NHR works, though he suggests Malta instead. Further, in his long experience he's never seen the Portugal tax office come after NHR people using the permanent establishment criteria. That's not saying they won't in the future but generally he believes if you are a small fish you have little to worry about. I am already set up in Bulgaria but I find the costs too expensive. I will set up another company for my girlfriend in Estonia and see how it goes.

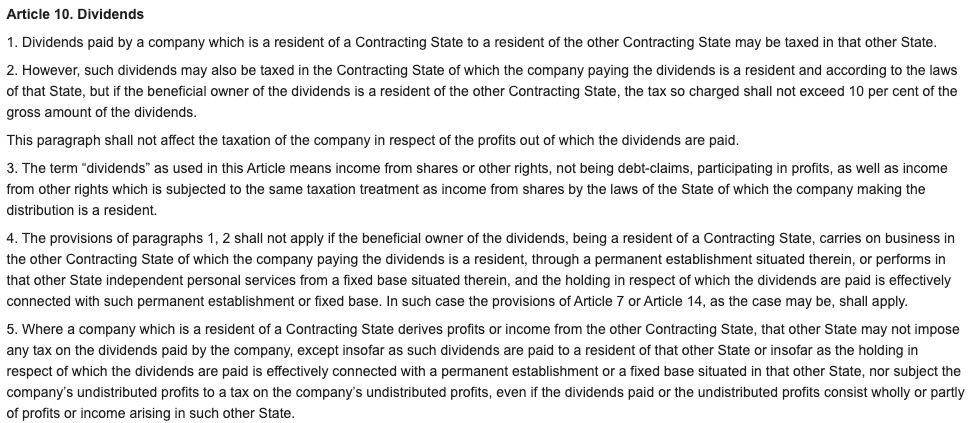

The tax treaty seems to suggests a reduction in taxes from the 20% of distributed dividends, to 10%. But I may be misreading that.

@JC1984 What would they consider a small fish? An annual profit of €100K? €500K?

I imagine under 10 million. Just a guess.

Typo: 1 million not 10I imagine under 10 million. Just a guess.

Last edited:

Here is the answer from the Estonian tax authorities regarding the tax treaty with Portugal:

Thank you for contacting us.

Tax treaty does not reduce the level of taxation on Estonian corporate dividend distributions from the standard 20% rate to 10%, because it is the corporate income tax paid by the company. Tax treaty applies to income tax withheld from the beneficial owner, from you as the Portugese resident.

Please find next explanation on our website: Tax liabilities of companies established by e-residents | Estonian Tax and Customs Board

If an e-resident owner of an Estonian resident company receives a dividend, it necessary to draw a distinction between the income tax applicable to a dividend of an Estonian company and income tax withheld on a natural person’s dividend income. If an Estonian company pays income tax on dividends at the normal rate of 20/80, no further income tax withholding will apply for the dividend distribution to a natural (e-resident) person. An e-resident natural person in most cases will not be able to use income tax paid by an Estonian company for the purposes of double taxation relief in their own country of residency because the Estonian income tax was paid by a different person.

From the year 2019, dividends paid regularly by an Estonian company are subject to a lower rate of 14/86. In the latter case the Estonian company will withhold a further 7% on a non-resident natural person’s dividend income upon making a dividend distribution. Income tax withheld on dividends (7%) is an income tax rate applicable to natural person dividend recipients in Estonia that can be used for double taxation relief in the dividend recipient’s country of residency, depending upon such country’s rules and the tax treaty for the prevention of double taxation of income.

Best Regards,

Katrin Kullamaa

Consultant

Thank you for contacting us.

Tax treaty does not reduce the level of taxation on Estonian corporate dividend distributions from the standard 20% rate to 10%, because it is the corporate income tax paid by the company. Tax treaty applies to income tax withheld from the beneficial owner, from you as the Portugese resident.

Please find next explanation on our website: Tax liabilities of companies established by e-residents | Estonian Tax and Customs Board

If an e-resident owner of an Estonian resident company receives a dividend, it necessary to draw a distinction between the income tax applicable to a dividend of an Estonian company and income tax withheld on a natural person’s dividend income. If an Estonian company pays income tax on dividends at the normal rate of 20/80, no further income tax withholding will apply for the dividend distribution to a natural (e-resident) person. An e-resident natural person in most cases will not be able to use income tax paid by an Estonian company for the purposes of double taxation relief in their own country of residency because the Estonian income tax was paid by a different person.

From the year 2019, dividends paid regularly by an Estonian company are subject to a lower rate of 14/86. In the latter case the Estonian company will withhold a further 7% on a non-resident natural person’s dividend income upon making a dividend distribution. Income tax withheld on dividends (7%) is an income tax rate applicable to natural person dividend recipients in Estonia that can be used for double taxation relief in the dividend recipient’s country of residency, depending upon such country’s rules and the tax treaty for the prevention of double taxation of income.

Best Regards,

Katrin Kullamaa

Consultant

Tax treaty does not reduce the level of taxation on Estonian corporate dividend distributions from the standard 20% rate to 10%, because it is the corporate income tax paid by the company.

Well at least now you know that your PT doesn't have a clue.

Interesting.If you don't live for 183 days in PT then you could pair your NHR with a US LLC.

You only need to rent an apartment in PT t be considered tax reisdent there so If you don't stay long enough in PT to trigger a permanent establishent then it could work but you have to double chck with a Portuguese lawyer.

In theory it works.

1. Is the 183 days really the main factor here? Not sure about PT but other EU countries consider a company a local tax resident if it is effectively managed from the country at any time during the year.

2. Assuming this structure works in PT, you would have to make sure not to spend more than 183 days in any other country? Plus there is still the risk that the other countries where you stay consider the US LLC local and tax it

Is the 183 days really the main factor here?

Well, i said 183 days because usually it's the time after which you trigger PE.

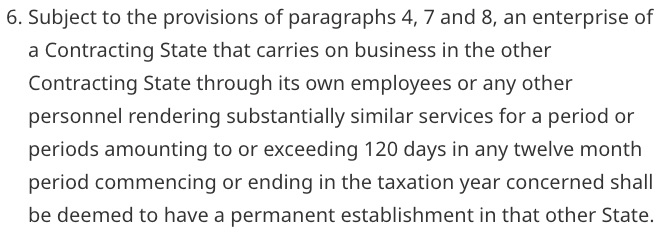

If you want to go ahead with this structure you have to analyze DTT between PT and the other countries where you plan to stay. Usually under article 5 it says how many days to permanent establishment

For example in the DTT between Canada and PT it's 120 days.

In Switzerland otherwise it's 30 days.

other EU countries consider a company a local tax resident if it is effectively managed from the country at any time during the year.

The question here is: how would they know? Let's say you have EU passport and rent a Swiss holday home for the entire year. You could spend up to 90 days every 6 months.

How would they know that during that time you didn't work from your laptop?

They can't.

you would have to make sure not to spend more than 183 days in any other country?

You have to make sure to not trigger PE in the countries you plan to stay and you'll discover in the DTT between PT and the countries you plan to stay after how many days the DTT is triggered.

Plus there is still the risk that the other countries where you stay consider the US LLC local and tax it

See the answer above.

Well, i said 183 days because usually it's the time after which you trigger PE.

If you want to go ahead with this structure you have to analyze DTT between PT and the other countries where you plan to stay. Usually under article 5 it says how many days to permanent establishment

For example in the DTT between Canada and PT it's 120 days.

In Switzerland otherwise it's 30 days.

The question here is: how would they know? Let's say you have EU passport and rent a Swiss holday home for the entire year. You could spend up to 90 days every 6 months.

How would they know that during that time you didn't work from your laptop?

They can't.

You have to make sure to not trigger PE in the countries you plan to stay and you'll discover in the DTT between PT and the countries you plan to stay after how many days the DTT is triggered.

See the answer above.

Thanks @Marzio

I think the first thing to get clarity on is whether PT would consider the US LLC a local tax resident.

For that we would need to check what PT tax law says. That piece of info I am missing now

Now we'd have two scenarios:

1. PT does NOT consider the US LLC local tax resident

2. PT DOES consider the US LLC local tax resident

Under scenario 1 you are fine with PT. If the US LLC is single member and not ETBUS, no tax in the US and you would have to analyze what happens with other countries you'll be staying during the year.

Under scenario 2, the DTT would play a role, theoretically. I still have doubts on this since the DTT is relevant when a (legal) person is liable for tax in both signing states; a single member US LLC is however a pass-through and disregarded entity in the US and you will not get a certificate of tax residence from the IRS. If the US LLC is not a tax resident of the US then the DTT cannot help and you are on the hook in Portugal.

Even if the DTT were to be invoked, the PT-USA treaty reads as follows for PE:

Then there's a clause similar to the one you cite for Canada-PT:

But in my opinion this clause 4 does NOT mean that you need any of the points in clause 2 for 9 months. It just describes another situation in which you would trigger PE. I.e., even if you do not have any of a) to f) in 2. in PT, you can still trigger PE if for instance you have employees working in PT from their home for over 9 months.

The way I see it, if you stay for a couple of months in PT and you manage the US LLC from there, you are creating a PE in PT. Another discussion is what part of the US LLC profits would be taxable in PT.

This reasoning would generally be applicable to other countries you stay in, so you'd be at risk of triggering (partial) PE in all of them.

in my opinion clause 4 does NOT mean that you need any of the points in clause 2 for 9 months.

Any element from (a) to (f) could trigger a permanent establishment.

Elements from (b) to (f) are physical in nature and they trigger a PE becase of their supposed fixed nature.

I mean you don't set up a mine for less than 9 months right? Or a branch, or an office, or a factory.

Place of management instead isn't fixed in nature so imho it can't trigger a PE immediately, there needs to be some "time to permanent establishment"

Imagine ths situation: you are tax resident under NHR because you rented an apartment for the year and you spend 5 days in PT while the remaining 360 days you spend 90 days in 4 countries.

Put aside the fact that the other countries could claim you are creating a PE there, imagine that this wouldn't be the case.

Are you creating a PE in PT?

Clause 4 indeed means that if your situation doesn't fit any of the elements from (a) to (f) you are creating a PE in PT if you carry out a business from PT for a period of 9 months in any 12 months period.

I agree it wouldn't sound very logical to have a PE in PT in that case but assumptions based on common sense are not necessarily aligned with what the law says. Check out the example of Greece:Imagine ths situation: you are tax resident under NHR because you rented an apartment for the year and you spend 5 days in PT while the remaining 360 days you spend 90 days in 4 countries.

Put aside the fact that the other countries could claim you are creating a PE there, imagine that this wouldn't be the case.

Are you creating a PE in PT?

For determining a legal entity as being tax resident in Greece, the exercise of effective management in Greece for any period during the tax year is sufficient.

https://taxsummaries.pwc.com/greece/corporate/corporate-residence

Again, I am not sure what the PT law says.

If the law of the country does not clearly establish a minimum number of days for effective management to trigger PE, I think there would be a significant risk of the company being liable to tax in that country if you spend time there.

Additionally, CFC could be a problem too for a US LLC not taxed in the US:

https://taxsummaries.pwc.com/portugal/corporate/group-taxationProfits or income derived by an entity resident in a black-listed jurisdiction, or in a jurisdiction where it is subject to an effective taxation below 50% of the taxation that would have been applied if such entity was resident for tax purposes in Portugal, are imputed to the Portuguese taxpayer, provided it holds, directly or indirectly, at least 25% of the share capital, voting rights, or rights on income or assets of that entity. Upon distribution of the profits, a deduction is available for previously imputed income.

I've both read that CFC rules in PT are applicable

a) to both active and passive income and

b) only if 25% or more of the company's income is passive

If b) is correct, CFC would not be a problem.

How likely this is to be enforced by the PT tax authority is another matter.

We could go on and on speculating, i know that there are people that are getting away with a US LLC + NHR. Don't know if it's because PT tax administration doesn't care or they are preparing a giant mousetrap at the end of their NHR 10 years.

I also know people that are UK LTD directors and only shareholders receiving tax free dividends while living in PT. Now it's less attractive of a solution because ot the UK CIT increase to 25% but until yesterday they paid 19% total tax and the LTD was 100% managed from PT.

I also know people that are UK LTD directors and only shareholders receiving tax free dividends while living in PT. Now it's less attractive of a solution because ot the UK CIT increase to 25% but until yesterday they paid 19% total tax and the LTD was 100% managed from PT.

Share:

Latest Threads

-

-

-

Mentor Group Gold - AD Thread! Panama-Based SVM: Making Stablecoin Business Solutions Simple

Mentor Group Gold - AD Thread! Panama-Based SVM: Making Stablecoin Business Solutions Simple- Started by palandrome

- Replies: 5

-

What's the maximum you would keep with CIM Banque (CH)?

- Started by response67red

- Replies: 9