"All legal documents and company-related paperwork should remain in the Cyprus office or be accessible in the office at any time if they are uploaded to cloud data systems." - wohoo...back to the eighties...No worries.

After reading the replies you got which are misleading. I would say get proper tax advice before you land yourself in hot water. Your activity is "Holding business" so you are directly impacted. GAAR is real. Please read the below link fully. You otherwise risk losing tax treaty benefits. Don't rely on bro science here.

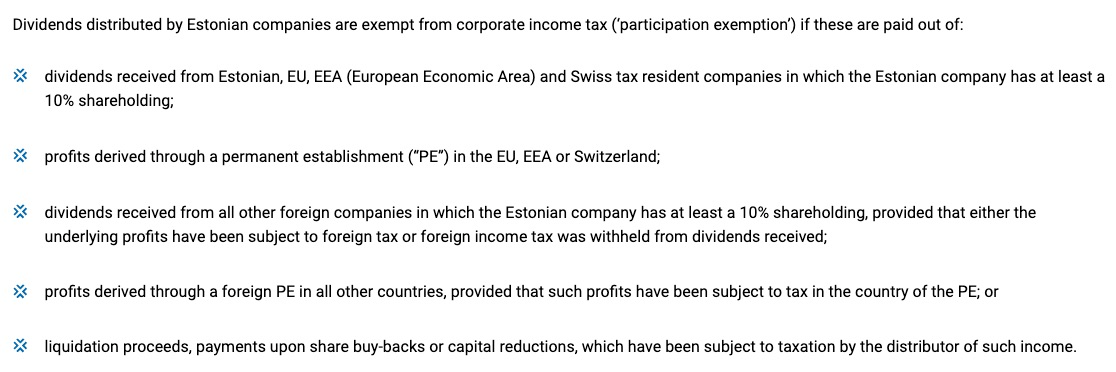

The Importance of Economic Substance for EU Companies

https://aspentrust.com/the-importance-of-economic-substance-for-eu-companies/

After you read it then....read it again. Have a nice evening.

") So, if there is a laptop in the office that is always connected to the Dropbox accounting and agreement folder, problem solved...or? Just a funny writing...

So, if there is a laptop in the office that is always connected to the Dropbox accounting and agreement folder, problem solved...or? Just a funny writing... It feels like the article just shows different way's of proving presence and there are many ways of doing that, some are more creative then other. The key point is that as long as the corp taxes are paid locally, you don't try to outsource (too much) of the administrative work (eg. keep it in the original country jurisdiction) you will be fine. Of course, keeping an arms length is the best way in regards to management, which they also mention in the article.

Yes, the presence requirement would need to be solved in an adequate way...and of course, it only complicates it some more. But it's not like you need to over complicate and hire a huge staff of employees and put them in a big corp building to prove presence. On the other hand, if you would hire a big staff and get a big corp building paid by the dividend that was already taxed once...who will benefit from that? Exactly, the local jurisdiction

So, of course they try to scare you. More money to the politicians (just because they missed a loophole the first time)

As always, laws change and as you already recommended; a local tax lawyer is always a must as well as a local (good!) CA/CPA, I would say.

ps. The article is written by a company that makes money helping companies pass the presence test...it's a little biased, I would say. Sounds just like an American insurance company..."if you don't do it like we say, and we are not saying you should, but who knows what trouble you might get into. Pay us, but we don't guarantee anything..."

Regarding the article. The footer says:"All legal documents and company-related paperwork should remain in the Cyprus office or be accessible in the office at any time if they are uploaded to cloud data systems." - wohoo...back to the eighties...

It feels like the article just shows different way's of proving presence and there are many ways of doing that, some are more creative then other. The key point is that as long as the corp taxes are paid locally, you don't try to outsource (too much) of the administrative work (eg. keep it in the original country jurisdiction) you will be fine. Of course, keeping an arms length is the best way in regards to management, which they also mention in the article.

Yes, the presence requirement would need to be solved in an adequate way...and of course, it only complicates it some more. But it's not like you need to over complicate and hire a huge staff of employees and put them in a big corp building to prove presence. On the other hand, if you would hire a big staff and get a big corp building paid by the dividend that was already taxed once...who will benefit from that? Exactly, the local jurisdiction

As always, laws change and as you already recommended; a local tax lawyer is always a must as well as a local (good!) CA/CPA, I would say.

ps. The article is written by a company that makes money helping companies pass the presence test...it's a little biased, I would say. Sounds just like an American insurance company..."if you don't do it like we say, and we are not saying you should, but who knows what trouble you might get into. Pay us, but we don't guarantee anything..."

Copyright © 2023 Aspen Trust Group | Privacy Policy | Cookie Policy | Legal Notice

Designed by Tenba Group

Click on the Tenba Group-link and you get to a company doing Chinese SEO

Last edited: