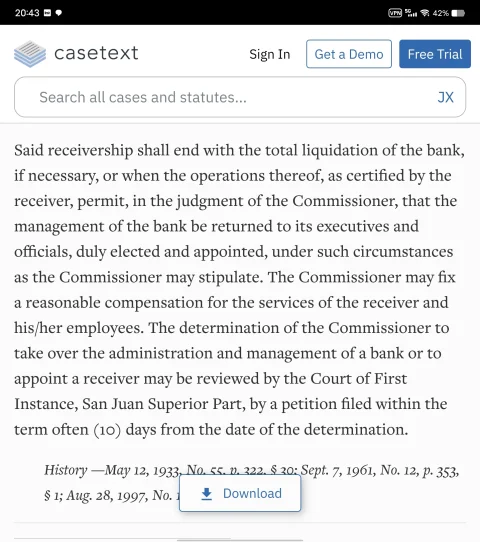

This is the interesting part, but it's up to the Commissioner. But it can be reviewed by the court.

Our valued sponsor

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Euro Pacific bank is a scam

- Thread starter OffshoreCorpTalk

- Start date

-

- Tags

- euro pacific bank

Puerto Rico’s banking system operates under a mix of federal and local laws. As an unincorporated territory of the United States, Puerto Rico’s banking sector is subject to US federal banking regulations

OCIF of PR has closed down quite several banks recently and also during the past years, just wonder have the clients received their savings.

OCIF of PR has closed down quite several banks recently and also during the past years, just wonder have the clients received their savings.

Last edited:

Puerto Rico’s banking system operates under a mix of federal and local laws. As an unincorporated territory of the United States, Puerto Rico’s banking sector is subject to US federal banking regulations

OCIF of PR has closed down quite several banks recently and also during the past years, just wonder have the clients received their savings.

how many banks and which ones were closed down recently ?

EPB had nothing to do with the robbery. It was robbed just like its customers. Since I'm the only shareholder I was robbed too. But Mark Anderson, a former shareholder, was robbed of his life. At least we still have ours.One of the most corrupt places on earth according the officially published information. OCIF, Receiver, EPB. It is just a perfect well prepared robbery and we cannot do anything.

The Commissioner order the total liquidation of the bank, then the dissolution of the parent company. It will never be returned to my control. It will be completely erased from existence. That is what the Commissioner insisted on.This is the interesting part, but it's up to the Commissioner. But it can be reviewed by the court.

EPB had nothing to do with the robbery. It was robbed just like its customers. Since I'm the only shareholder I was robbed too. But Mark Anderson, a former shareholder, was robbed of his life. At least we still have ours.

The Commissioner order the total liquidation of the bank, then the dissolution of the parent company. It will never be returned to my control. It will be completely erased from existence. That is what the Commissioner insisted on.

The fact that they are not keeping us informed of anything shows how little the Commissioner cares about EPB and its Customers.

I would really like to speak to that woman and tell her about the consequences that her actions are having in my life.

I know another customer of EPB who just got a personal loan from his local bank so he can pay for his insulin, he asked me to loan him money until he gets his money back from EPB but unfortunately I couldn't help him, I'm just as broke as he is, I'm waiting for my home to get sold.

Bank Liquidation Rules

In Puerto Rico, bank liquidation involves the appointment of a receiver, typically the FDIC, to manage the institution’s assets, liabilities, and operations. The receiver is responsible for maximizing the value of the failed bank’s assets, resolving its liabilities, and distributing any proceeds to creditors according to their priority rankings.Account holders of a failed bank in Puerto Rico can take several steps to safeguard their position during statutory administration, deposit insurance, and bank liquidation:

- Maintain accurate records of deposits, account balances, and transactions.

- Keep personal information up to date with the bank to facilitate communication during the resolution process.

- Monitor the financial health of the bank, and consider diversifying deposits across multiple institutions.

- Stay informed about FDIC deposit insurance limits and coverage.

- Respond promptly to any notifications or instructions from the OCFI, FDIC, or appointed receiver during the resolution process.

Legal Floris LLC

Telephone:001 646 513 2855 – USA

00371 678 81974 – Latvia

00357 25 057 544 – Cyprus

00352 20 301970 – Luxembourg

Registered office:

1013 Centre Rd. Suite 403-A

Wilmington, 19805

Delaware – USA

Cyprus office:

3 Zenonos Kiteos

2406 Nicosia – Cyprus

Postal address:

PO Box 50472

3605 Limassol – Cyprus

Bank Liquidation Rules

In Puerto Rico, bank liquidation involves the appointment of a receiver, typically the FDIC, to manage the institution’s assets, liabilities, and operations. The receiver is responsible for maximizing the value of the failed bank’s assets, resolving its liabilities, and distributing any proceeds to creditors according to their priority rankings.

Account holders of a failed bank in Puerto Rico can take several steps to safeguard their position during statutory administration, deposit insurance, and bank liquidation:

- Maintain accurate records of deposits, account balances, and transactions.

- Keep personal information up to date with the bank to facilitate communication during the resolution process.

- Monitor the financial health of the bank, and consider diversifying deposits across multiple institutions.

- Stay informed about FDIC deposit insurance limits and coverage.

- Respond promptly to any notifications or instructions from the OCFI, FDIC, or appointed receiver during the resolution process.

Legal Floris LLC

Telephone:

001 646 513 2855 – USA

00371 678 81974 – Latvia

00357 25 057 544 – Cyprus

00352 20 301970 – Luxembourg

Registered office:

1013 Centre Rd. Suite 403-A

Wilmington, 19805

Delaware – USA

Cyprus office:

3 Zenonos Kiteos

2406 Nicosia – Cyprus

Postal address:

PO Box 50472

3605 Limassol – Cyprus

EPB is not FDIC, there are only 5 or 6 banks in Puerto Rico that are FDIC.

Legal Framework for Creditors Impacted by Bank Failure in Puerto Rico

Creditors impacted by a bank failure in Puerto Rico can utilize the legal framework to recover their money. As mentioned earlier, the Puerto Rico Financial Institutions Act provides the basis for bank insolvency procedures and establishes the hierarchy of claims in the liquidation process. To maximize their chances of recovery, creditors should:- Stay informed about the insolvency proceedings and the actions taken by the receiver.

- File a proof of claim with the receiver to ensure their claim is recognized and properly prioritized.

- Monitor the liquidation process and participate in creditor meetings, if applicable.

- Consult with legal counsel to navigate the complex insolvency process and protect their interests.

Ye it is sad indeed, that EPB is not covered by FDIC. Otherwise I could not be worried at all.

Well when EPB was put into receivership it had no loans outstanding, and didn't have any debts. The only creditors where the depositors, and that was millions in excess cash available to pay them. The only assets the bank had other than cash were gold in its hedge book, and a $500K receivable from Currency Matters, a UK company in bankruptcy. The Receiver blew that Receivable by refusing to answer the simple questions asked by the liquidator. I answered them, but the liquidator insisted the answers come from the receiver, which despite my efforts, he never supplied.Bank Liquidation Rules

In Puerto Rico, bank liquidation involves the appointment of a receiver, typically the FDIC, to manage the institution’s assets, liabilities, and operations. The receiver is responsible for maximizing the value of the failed bank’s assets, resolving its liabilities, and distributing any proceeds to creditors according to their priority rankings.

Account holders of a failed bank in Puerto Rico can take several steps to safeguard their position during statutory administration, deposit insurance, and bank liquidation:

- Maintain accurate records of deposits, account balances, and transactions.

- Keep personal information up to date with the bank to facilitate communication during the resolution process.

- Monitor the financial health of the bank, and consider diversifying deposits across multiple institutions.

- Stay informed about FDIC deposit insurance limits and coverage.

- Respond promptly to any notifications or instructions from the OCFI, FDIC, or appointed receiver during the resolution process.

Legal Floris LLC

Telephone:

001 646 513 2855 – USA

00371 678 81974 – Latvia

00357 25 057 544 – Cyprus

00352 20 301970 – Luxembourg

Registered office:

1013 Centre Rd. Suite 403-A

Wilmington, 19805

Delaware – USA

Cyprus office:

3 Zenonos Kiteos

2406 Nicosia – Cyprus

Postal address:

PO Box 50472

3605 Limassol – Cyprus

The bank did have normal bills to pay, but none were past-due. Plus there was plenty of cash available to pay them . The only long-term obligation the bank had was its office lease, but that ended Dec. 2022. I was able to get out of the lease about three months early, and I sold the furniture for $50K, which went into the bank's checking account. So there was really nothing for the Receiver to do put pay the depositors back their money, and pay the outstanding bills using the funds in the bank's checking account. I negotiated discounts on the larger bills, and asked the bank's staff to pay every one. But the Receiver refused to allow the staff to pay the bills. He insisted on reviewing each bill and paying them himself. At this point I still don't know if anyone got paid. I think the only one getting paid is the Receiver.

If you are looking to blame someone blame The OCIF Commissioner. This is all her doing. There was no reason to put the bank into receivership. She didn't want the bank to exist due to my bad global reputation, that resulted from the 60 Minutes defamation. She turned down the sale to Qenta due to my 4.15% ownership of Qenta stock. But since she revoked the bank's license by refusing to renew it, even though the bank submitted the annual renewal on time (the bank was fined $700K for operating without a license, for all the days the bank believed its license was renewed, as no one at OCIF said a word to anyone that the license renewal was not accepted.) there was no need for receivership. Without a license I would have closed the bank on my own, returned all the deposits, paid the bills, and kept the remaining assets for myself. Novo only became an issue due to the unnecessary press conference the Concessioner called that allowed the international media to falsely claim the bank was shut down as a result of the J5 investigation for tax evasion and money laundering.

Last edited:

Well when EPB was put into receivership it had no loans outstanding, and didn't have any debts. The only creditors where the depositors, and that was millions in excess cash available to pay them. The only assets the bank had other than cash were gold in its hedge book, and a $500K receivable from Currency Matters, a UK company in bankruptcy. The Receiver blew that Receivable by refusing to answer the simple questions asked by the liquidator. I answered them, but the liquidator insisted the answers come from the receiver, which despite my efforts, he never supplied. The bank did have normal bills to pay, but none were past-due. Plus there was plenty of cash available to pay them . The only long-term obligation the bank had was its office lease, but that ended Dec. 2022. I was able to get out of the lease about three months early, and I sold the furniture for $50K, which went into the bank's checking account. So there was really nothing for the Receiver to do put pay the depositors back their money, and pay the outstanding bills using the funds in the bank's checking account. I negotiated discounts on the larger bills, and asked the bank's staff to pay every one. But the Receiver refused to allow the staff to pay the bills. He insisted on reviewing each bill and paying them himself. At this point I still don't know if anyone got paid. I think the only one getting paid is the Receiver. If you are looking to blame someone blame The OCIF Commissioner. This is all her doing. There was no reason to put the bank into receivership. She didn't want the bank to exist due to my bad global reputation, that resulted from the 60 Minutes defamation. She turned down the sale to Qenta due to my 4.15% ownership of Qenta stock. But since she revoked the bank's license by refusing to renew it, even though the bank submitted the annual renewal on time (the bank was fined $700K for operating without a license, for all the days the bank believed its license was renewed, as no one at OCIF said a word to anyone that the license renewal was not accepted.) there was no need for receivership. Without a license I would have closed the bank on my own, returned all the deposits, paid the bills, and kept the remaining assets for myself. Novo only became an issue due to the unnecessary press conference the Concessioner called that allowed the international media to falsely claim the bank was shut down as a result of the J5 investigation for tax evasion and money laundering.

Obviously the Receiver is going to insist on doing everything by himself, more time spent on silly things is more money that he can charge the bank.

These events don't happen that frequently so he needs to take advantage of everything opportunity, it's pure corruption!

A couple more weeks and it will be a Year since the bank was closed, unbelievable!

Plus, when I told the Commissioner that I was looking for a buyer for the bank, as the bad publicly about me made it impossible for me to own a bank, she told me that if I could not find a buyer that she would let me liquidate the bank myself. She assured me that she would never put the bank into Receivership. I wanted to avoid the very thing that has been happening for the past year, and at the time, so did the Commissioner.Obviously the Receiver is going to insist on doing everything by himself, more time spent on silly things is more money that he can charge the bank.

These events don't happen that frequently so he needs to take advantage of everything opportunity, it's pure corruption!

A couple more weeks and it will be a Year since the bank was closed, unbelievable!

Unfortunately there's no point in us keep talking about what should have happened. We agree the bank should never have been put in to Receivership.

The question is what can customers do now to protect their interests.

Do you have any new information as to what is happening? It's all gone quiet.

I will try to call the lawyer I spoke to last week.

The question is what can customers do now to protect their interests.

Do you have any new information as to what is happening? It's all gone quiet.

I will try to call the lawyer I spoke to last week.

I was told by Qetna's in-house counsel that they are finally making some progress with OCIF and the receiver. But I'm not sure exactly what progress has been made.Unfortunately there's no point in us keep talking about what should have happened. We agree the bank should never have been put in to Receivership.

The question is what can customers do now to protect their interests.

Do you have any new information as to what is happening? It's all gone quiet.

I will try to call the lawyer I spoke to last week.

Plus, when I told the Commissioner that I was looking for a buyer for the bank, as the bad publicly about me made it impossible for me to own a bank, she told me that if I could not find a buyer that she would let me liquidate the bank myself. She assured me that she would never put the bank into Receivership. I wanted to avoid the very thing that has been happening for the past year, and at the time, so did the Commissioner.

I guess the J5 must have pressured her to put the bank into Receivership or something else happened that made her change her mind.

At the end of the day what she did has proven to be disastrous for the bank and the customers, which doesn't make sense as the main job of a Commissioner is to protect the customers, not to destroy their lives.

I also think the pressure on the J-5 came for 60 Minutes Australia. So if I never filed my defamation lawsuit, none of this likely would have happened, the sale to Qetna would have been approved as initially supported by the Commissioner, no customer would have been inconvenienced, and I would have received $25 million from the sale of the bank.I guess the J5 must have pressured her to put the bank into Receivership or something else happened that made her change her mind.

At the end of the day what she did has proven to be disastrous for the bank and the customers, which doesn't make sense as the main job of a Commissioner is to protect the customers, not to destroy their lives.

Let’s look forward and not discuss the past, what is not relevant at all.

I could not personally trust any unknown lawyers in PR, as none of them will turn against the state. PR is pretty small country, everybody knows each other and media is also under control of state.

I could not personally trust any unknown lawyers in PR, as none of them will turn against the state. PR is pretty small country, everybody knows each other and media is also under control of state.

Last edited:

Share:

Latest Threads

-

-

Driver’s License in the Philippines – Fast and Painless

- Started by Overtrade

- Replies: 1

-

Remote Company Formation Options for Sanctioned Country IT Professional with Minimal Bureaucracy and Zero Local Taxes

Remote Company Formation Options for Sanctioned Country IT Professional with Minimal Bureaucracy and Zero Local Taxes- Started by IllIlllIII

- Replies: 1

-

-

Seeking Offshore Capital Partner for Short-Term Private Operation

Seeking Offshore Capital Partner for Short-Term Private Operation- Started by user12345

- Replies: 0